It is always interesting when two famous entrepreneurs disagree on something fundamental. In this case, it is Marc Andreessen and Peter Thiel. Here is Marc Andreessen’s recent tweet.

Something my friend & hero Peter Thiel and I vigorously disagree on: I *love* competition, I think it’s invigorating/stimulating/productive.

— Marc Andreessen (@pmarca) June 30, 2014

//platform.twitter.com/widgets.jsPut simply, Marc Andreessen is for competition and looks for opportunities that invite it while Peter Thiel is against it. Here is what he wrote in his new Zero To One book (based on these notes):

One way to tell whether you’ve found a good frontier is to answer the question “Why should the 20th employee join your company?” If you have a great answer, you’re on the right track. If not, you’re not. The problem is the question is deceptively easy sounding.

So what makes for a good answer? First, let’s put the question in context. You must recognize that your indirect competition for good employees is companies like Google. So the more pointed version of the question is: “Why would the 20th engineer join your company when they could go to Google instead and get more money and prestige?”

The right answer has to be that you’re creating some sort of monopoly business. Early businesses are driven by the quality of the people involved with them. To attract the best people, you need a compelling monopoly story. To the extent you’re competing with Google for talent, you must understand that Google is a great monopoly business. You probably should not compete with them at their core monopoly business of search. But in terms of hiring, you simply can’t compete with a great monopoly business unless you have a powerful narrative that has you becoming a great monopoly business too.

Thiel’s point is that you need to look for businesses that will be a monopoly in their market. And not just some pretend monopoly. Indeed, a monopoly that satisfies an economist’s definition: one where you have significant discretion over the price you charge. So you could be the monopoly provider of Thai food on a street but that isn’t a real monopoly because if you raise your price people will go to other restaurants on the street. Indeed, in his book, Thiel articulates a way of telling that you are in a monopoly that is precisely the way an anti-trust economist would look at market definition (something that I will return to hopefully in a future post).

Now the disagreement between Andreessen and Thiel goes beyond just economic issues. One of them likes competing while the other really doesn’t. To each their own on that one. But on the economics and entrepreneurial strategy point I am not sure there is actually a fundamental disagreement. I think Thiel and Andreessen are talking about two different things: both of whom could be considered monopoly in the 100 percent of a market sense. Here is an exchange that illustrates the disagreement:

Peter Thiel: Are there some industries that are too dangerous to disrupt? Disruptive children go to the principal’s office. Disruptive companies like Napster can get crushed. Can you succeed with head-on competition, even if you have the Silicon Valley model in other respects?

Marc Andreessen: Look at what Spotify is doing, which is something very different than what Napster did. Spotify is writing huge checks to labels. The labels appreciate that. And Spotify put itself in position to write those checks from day one. It launched in Sweden first, for example, because it wasn’t a very big market for CDs. It’s a disruptive model but they found a way to soften the blow. When you start a conversation with “By the way, here’s some money,” things tend to go a little better.

It’s still a high-pressure move. They are running the gauntlet. The jury is still out on whether it’s going to work or not going forward. The guys on the content side are certainly pretty nervous about it. This stuff can go wrong in all kinds of ways. Spotify and Netflix surely know that. The danger in just paying off the content people is that the content people may just take all your money and then put you out of business. If you play things right, you win. Play them wrong, and the incumbents end up owning everything.

Many economists would read this and actually be on Thiel’s side. How do you build a business when others have market power and can use competition against you?

To answer this question, let’s begin by understanding the Thiel approach. What he wants entrepreneurs to do is seek out markets that they can dominate.

For a company to own its market, it must have some combination of brand, scale cost advantages, network effects, or proprietary technology. Of these elements, brand is probably the hardest to pin down. One way to think about brand is as a classic code word for monopoly. But getting more specific than that is hard. Whatever a brand is, it means that people do not see products as interchangeable and are thus willing to pay more. Take Pepsi and Coke, for example. Most people have a fairly strong preference for one or the other. Both companies generate huge cash flows because consumers, it turns out, aren’t very indifferent at all. They buy into one of the two brands. Brand is a tricky concept for investors to understand and identify in advance. But what’s understood is that if you manage to build a brand, you build a monopoly.

Scale cost advantages, network effects, and proprietary technology are more easily understood. Scale advantages come into play where there are high fixed costs and low marginal costs. Amazon has serious scale advantages in the online world. Wal-Mart enjoys them in the retail world. They get more efficient as they get bigger. There are all kinds of different network effects, but the gist of them is that the nature of a product locks people into a particular business. Similarly, there are many different versions of proprietary technology, but the key theme is that it exists where, for some reason or other, no one else can use the technology you develop.

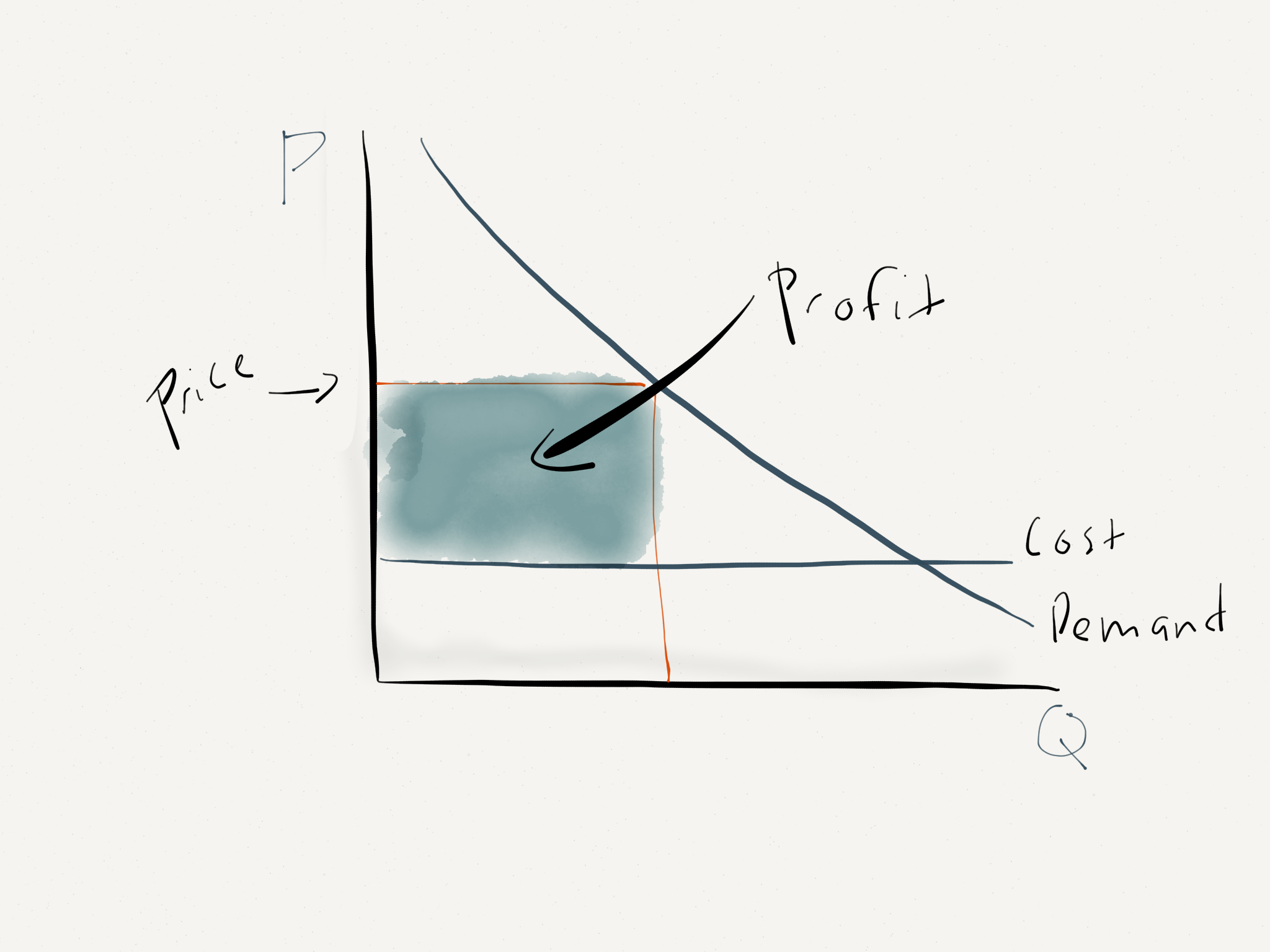

This is familiar. All of these are barriers to entry. This is monopoly that comes from you controlling scarce resources that no one else has control over. When this occurs, your pricing graph looks like the textbook monopoly case because your business faces a downward sloping demand curve.

Scott Stern and I have termed this approach to entrepreneurial strategy: investing for control. You achieve it by patiently building your business at the same time as ensuring that you will be insulated from future competition. It takes time and it takes investment dollars as resources. Put out some crappy minimum viable product and you lose some options to control because you have shown your hand to others. Instead, what you want to do is put out a complete product with a strategy to acquire the complementary resources to insulate it from future competition. This, for instance, is what Tanium appears to be doing.

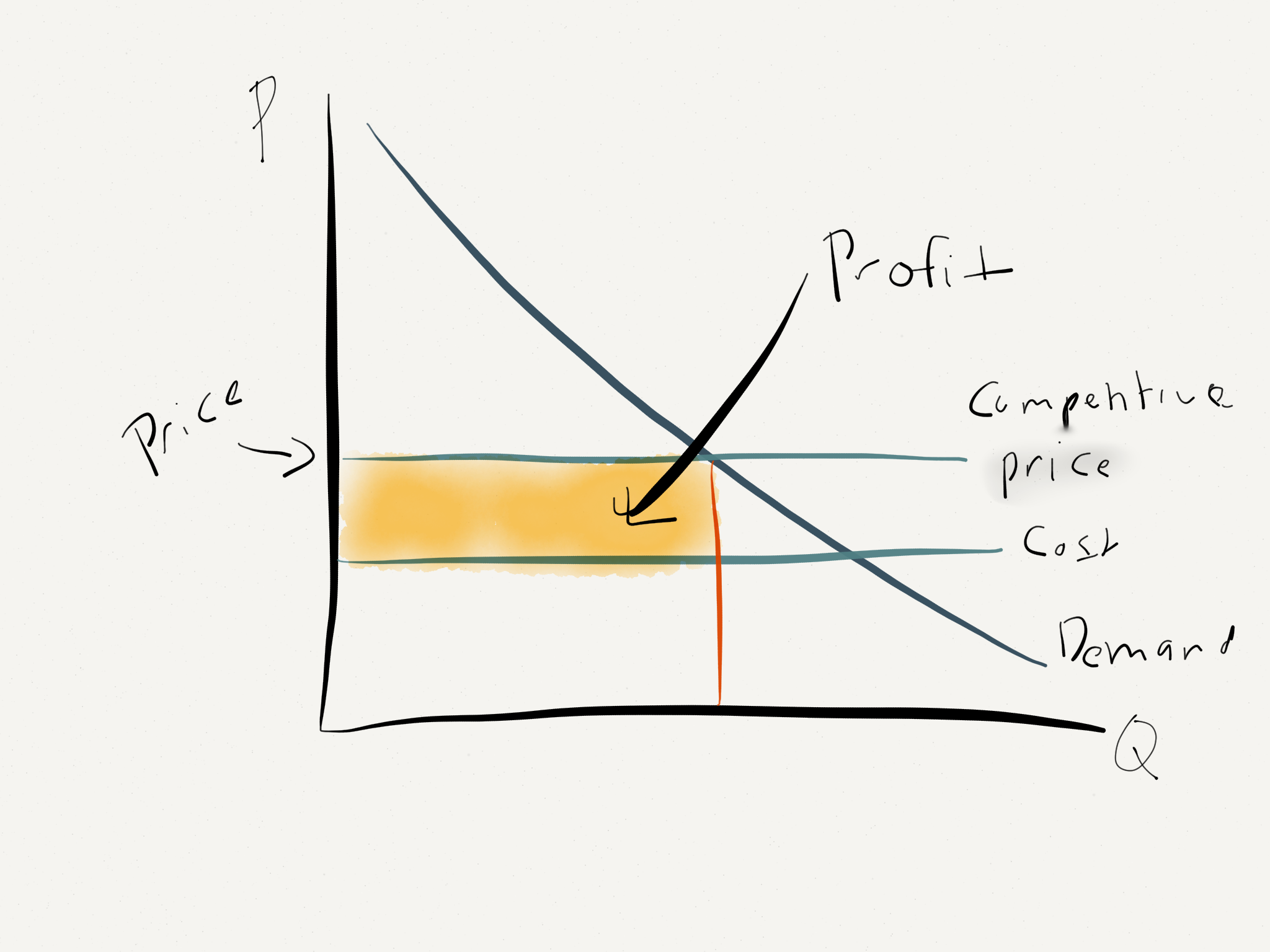

There is, however, another sort of monopoly — a path that gets you 100 percent of a real market. This is done by having the capabilities to beat all rivals on either quality or cost. To see how this arises consider a very structurally price competitive market (in economics, Bertrand competition). Now suppose that you develop an innovation that allows to have lower marginal costs than everyone else. In this situation, you will be able to capture 100 percent of the market and so you will be a technical monopoly. The difference is that you pricing is constrained by potential competition from other firms. In other words, your monopoly profits look like this:

We have termed this approach to entrepreneurial strategy: focusing on execution (something I have mentioned before). That’s a phrase entrepreneurs say alot but the economists and many business school professors roll their eyes at. I was one of them for many years. The reason is that we couldn’t see that they could do that (although there are many examples of people who have) and why they would want to do that when investing for control seems like a solid route to profits.

However, it is not so obvious that one path to monopoly is more profitable than the other. For starters, if you focus on execution you can get to market quicker and with fewer resources. You can learn as you go and actually invest for the capabilities that will give you a competitive advantage in the future. In other words, while it takes on-going work — no resting on your monopoly laurels here — you can still ‘own’ a market.

The point here is just as an entrepreneur can choose a strategy of competing versus cooperating with established firms, it can also choose between investing in control or focusing on execution. Which is the right path is hard to tell at the outset and it may be that a start-up will want to switch between strategies as it learns more; so long as that switch is feasible (something again for another post). So both Andreessen and Thiel can have different preferences regarding control versus execution and still both be right.

Not so different from the position approacah vs the resource-based approach discussion…Is it?

An adult human with an avatar from a South Park character generator? [pulls up two chairs to listen to what this very good person has to say]

I see why economists and business school professors roll their eyes at “focusing on execution”. Your second graph is complete nonsense.

In a competitive equilibrium, price equals to marginal cost. Hence, the higher horizontal curve in your second graph IS NOT THE COMPETITIVE PRICE, the lower one is, and that empty triangle to the right of the yellow rectangle is a dead weight loss. The logic of this is unassailable, and there is no sense in which this deviation from competitive pricing is ideal.