Yesterday, the folks at Andreessen-Horowitz released a slide deck on their reasoning why “this time it is different” on tech funding and bubbles. It is worth a little of your time but here are the take aways:

Yesterday, the folks at Andreessen-Horowitz released a slide deck on their reasoning why “this time it is different” on tech funding and bubbles. It is worth a little of your time but here are the take aways:

- The amount of money going into tech start-ups is still much less than it was in the dot.com bubble of 2000. Indeed, as a share of GDP funding has been flat since that time. It is also flat as a function of people online.

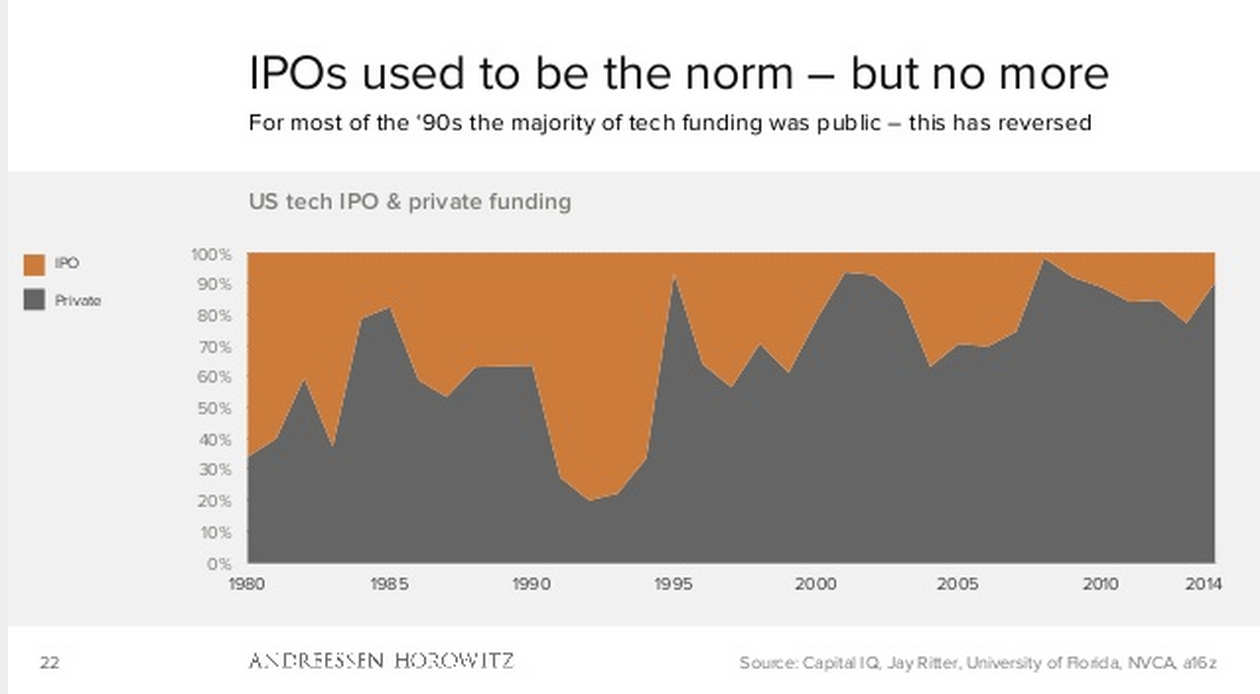

- IPOs are no longer a thing in tech and instead there has been a growth in late stage private funding. Most of these are coming from larger rounds for the big ‘billion dollar plus’ valuation companies.

- Earnings are rising so the companies being funded look alot more real than they did 15 years ago.

- There is a surge in early stage seed funding.

- Traditional investors in public markets have moved into late stage private funding.

This is a thought provoking issue. Partly, because the aggregate numbers seem to contradict the “word on the street” that funding for start-ups has never been easier and the valuation methodologies for companies are no better than before. Indeed, for seed rounds, it seems to me that investors have given up on valuation and invest because they like what they see. That said, in an arena dominated by Knightian uncertainty (that is, we have no way to work out what is going on), dropping the pretence of knowledge is a refreshing transparency.

So what to make of all this? I have a potted theory of what is going on (and it is not only potted but I don’t have real empirical evidence for it either). The theory is this:

- The tech funding is heavily geographically concentrated. We know that this is the case with entrepreneurial activity (see here) and I think it is becoming more so.

- That means that while an economy-wide view of funding shows flatness in the aggregates, I wonder if we did just a Silicon Valley analysis, it would look like this. My guess is that funding from Silicon Valley to Silicon Valley has increased.

- Given this, I think the heart of the move to earlier stage funding is doing hand in hand with the increase in wealth concentration. My narrative for this is as follows. People make money in tech. They don’t trust traditional investments since the Great Recession but they want to put their money somewhere. Socially, they hang out with other people in the area and what they talk about is who they have invested in. In other words, they are on the hunt for early stage companies to talk about at social gatherings and also as a means of “giving back.” (And I don’t mean that cynically but that this is an actual process).

- In other words, there is more money around and it is less grounded in real valuations but it is, in effect, a form of consumption. The great bit about that is that it is means that the traditional bubble issue — returns don’t come in, people panic and then they pull funding quickly — does not arise. Instead, the process hinges on the occasional hits even if the overall returns of a portfolio are lower than safer, more traditional investing.

My point is that if you want to understand tech investing today, sure, you could look at economics and finance as Andreessen-Horowitz are doing but my feeling (and it is a feeling) is that it misses a critical social context. Add that into the mix and we may be able to obtain a better understanding of precisely what is going on and whether, in fact, it is different this time.