For IEEE Micro, July-August.

The corona virus turned crowded places into transmission hot spots. Coffee shops, popular restaurants, and arenas closed in the United States in March, along with dentist offices, schools, and other places where super-spreading took place. Shelter-in-place mandates went into effect starting on March 17 in many states, and more than forty states instituted such orders by the end of March. As the first wave of infection receded, some areas partially opened up activities, and, as of this writing, more is expected.

Many commentators call these events unprecedented. There has been nothing like them since the flu pandemic of 1918-19. Does that imply we are in new economic territory in which economic analysts do not know what is happening, nor why? That question matters because it informs predictions about what is likely to happen in the next year.

Here is an outline of the answer, which is the topic for today’s column. The arrival of the virus has caused one broad barometer of economic activity – consumer spending – to fall more in a single month than in any prior month in US history. As an economic fact, this decline deserves the label “without precedent.”

Subsequent events have followed the textbooks about how one part of the economy links with other parts. Everyone swims in the same water, and while the currents in the technology sector have been rough, they are less rough than elsewhere.

Fear and Reallocation

The economics of the corona virus begins with one major behavior: Americans cut back on spending. The nationwide average decline in consumer spending in April was 13.6%, following more than 7% in March. Some consumers cut back on spending as a precaution. Others did not have any activity on which to spend their income. Many saved money by redirecting their free time to online activities.

The economic consequences were grim. Retail sales fell 16.4% in just April alone. That reflected a variety of experiences. Local ordinance forbid many businesses from serving physical customers. Online customers or curb-side pick-up made up for a fraction of it, and not everywhere.

Many of those employed in the hardest hit sectors – leisure and hospitality, retail, and construction – either lost their jobs or received furlough notices. As of this writing, approximately forty million people filed for some form of unemployment in March, April or May. While some of this unemployment was temporary – e.g., at the dentist and hardware store, some of it – e.g., at hotels, small restaurants, or an amusement park – will revive slowly, at best, as these businesses figure out whether anybody wants their services, and what they can provide, if any.

Official statistics do not tell the whole story. Some employment in services declined too – among undocumented workers, first-time seasonal employment, the informal sector (especially child care), and some gig economy jobs. Such activity typically does not get measured accurately. Most surveys indicate these sectors also had a grim experience.

More broadly, the US statistical apparatus for monitoring economic activity was not designed to measure such a rapid change. Even the economic declines of the dot-com bust in 2001 and financial crisis of 2008 unfolded more slowly than this. With that caveat stated, as of this writing, the official national unemployment rate stood at just north of 13%, with enormous variance across locations, and with an expectation that it will get better as different areas open up. It will take several months of data to perceive the trends with certainty.

The decline in consumption caused a second less visible and rather predictable issue: Many existing business took on debt involuntarily. No business was free of monthly expenses for rent, interest payments, and basic administrative costs, which could not be covered with missing revenue. If a business could not borrow money, then it had to take the cash out of savings.

That happened at the local beauty salon and barber, the division of Lyft, Groupon, and TripAdvisor, as well as at movie theaters, and virtually every big retailer. It also happened at hospitals, who redirected their resources to address the pandemic. (Full disclosure: I am married to a hospital-based physician.) None of this is sustainable, and it is especially problematic if the business already held large amounts of debt or little cash.

Government programs made the decline in consumer spending not as drastic as it would have been. Interest rates declined sharply, and Fed bought bonds, which infused liquidity into the economy, among other actions. In spite of some well publicized errors and biases, federal programs funneled cash to households and business, with some aimed at particular economic areas, such as the medical sector, and other programs exchanged loans for keeping employees on the payroll. That allowed some households and some businesses to put off painful decisions. Analysts and business journalists have not fully uncovered who benefited most and least, and whether any of it was scandalous. An open question, as I write, is whether there will be more such programs.

While much of the technology industry followed the rest of the economy into unpleasant times, the technology sector includes many visible positive economic experiences. Online streaming boomed for obvious reasons. The marketing divisions of Netflix and Hulu and Disney+ could not have asked for more users. The biggest (and already cash-rich) online companies – such as Google and Facebook – saw their online traffic grow, even as the value of their advertising dropped. Some parts of electronic retailing – Amazon, Walmart, Target and EBay – experienced large increases in sales. Deliveries from UPS and Fedex soared (and backed up). A few digital infrastructure firms found their capacity tested to the limits by spikes in traffic. Some cloud firms experienced their sunniest days.

If you work at one of the fortunate firms, count your blessings.

Causes and recovery

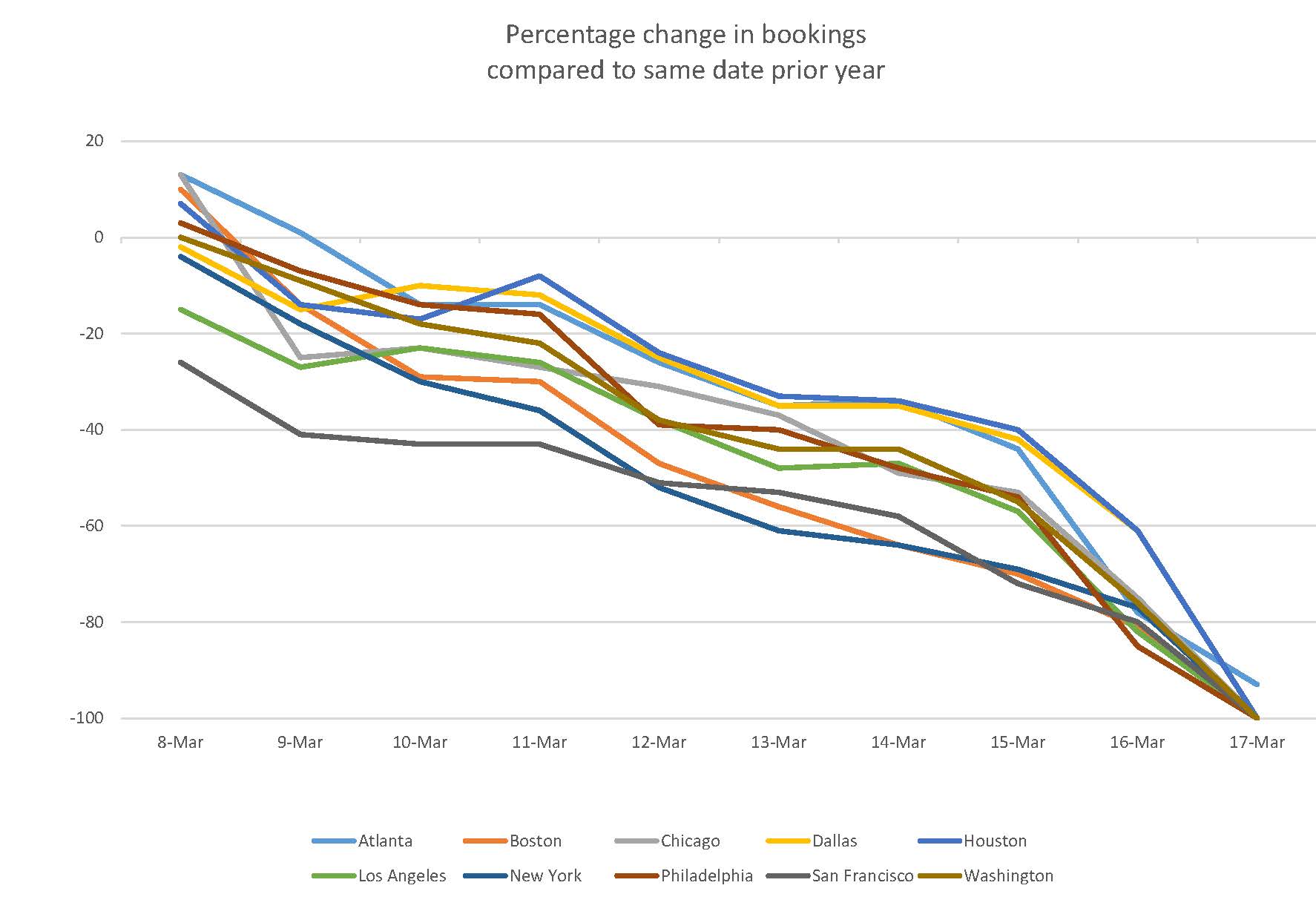

The drop in consumption motivated analysts to turn to non-traditional sources of information to track events. One example comes from data published by Open Table, who regularly tracks restaurant bookings and makes the data available (https://www.opentable.com/state-of-industry). The figure presents ten days of Open Table’s data for the major cities in the ten largest US metropolitan areas. It shows the percentage change in bookings for a sample of locations within these areas, compared with similar dates a year earlier.

Notice the timing. By the beginning of March the pandemic had begun to affect a few cities. As that awareness spread, bookings went down in advance of the stay-at-home orders. That was due to a decline in business travel and leisurely outings for social evenings. If we had graphs for other cities it would show the same thing. If we had graphs for dentist office visits, coffee shops, and clothing store shopping trips, we would see something similar. In other words, public orders ratified what would have substantially happened already.

There is no reason to expect the fear to entirely subside after orders are lifted. To be sure, some fearless young people will go to the beach and have a drink at a bar in any circumstance. To understand the alternative behavior, just talk to someone older. They might agree to a small outdoor picnic. My aging relatives are not itching to go out to the theater as they once did, and the theaters are closed anyway. Know anybody who has died from Covid-19? I do, and needless to say, the surviving relatives also are not itching for a night on the town.

Which is a long way of saying there is no chance consumer spending will return to 100% of its former level soon. Consumers will not come back in the same numbers, nor as frequently, and most states bar large gatherings in any event. Many business simply do not have the capacity to handle the same number of customers and also accommodate social distancing.

What next?

What is the most optimistic scenario for the economy? Every forecast contains a big question mark because some regions will experience a second wave of infection and a targeted shutdown, while others will not. It is not possible to know yet where, nor how bad until it actually happens. That said, most estimates today forecast that GDP for 2020 will decline at least 6 to 10% compared to 2019.

Vaccine development typically takes at least twelve to eighteen months. This one is on a rushed schedule, so let’s try to be optimistic and consider what happens if it shows up in January, 2021. What then?

Even if everyone can go back to work, the hangover should last. Many businesses need to pay their mortgages first, and will not bring employees back without sustained evidence of a recovery. For the same precautionary reasons, we should expect postponement in new capital investments.

In addition, government taxes have fallen. State and local government expenditure will decline for at least for one budgetary cycle. Want a local street repaired, more police on the street, or another teacher in the grade school? Most local governments will not have the funds.

What about the worst case scenario? That involves so much bad news I hope I do not have to put such details into words.

Copyright IEEE Micro. To read the original, see here.